China’s ADC Global Expansion: From Licensing to Technology Leadership

As a China-based pharmaceutical distributor serving global markets, DengYueMed has been closely tracking a major industry shift:

Chinese antibody-drug conjugates (ADCs) are rapidly expanding globally, transitioning from asset out-licensing to technology-driven collaboration.

As of early 2026:

- ~44 ADC-related deals completed

- Total disclosed value exceeds $53.2 billion

- Over $3.1 billion upfront payments

More importantly, deal structures are evolving:

- Single-asset licensing → multi-asset partnerships

- Product export → platform-level collaboration

I. A Three-Phase Evolution of China’s ADC Globalization

Phase 1 (2019–2021): Late-Stage Asset Licensing

A landmark deal:

- RemeGen → Seagen (~$2.6B)

Key characteristics:

- Late-stage / near-commercial assets

- Mature clinical data

- Low risk for global partners

➡️ China acted mainly as an asset provider

Phase 2 (2022–2024): Pipeline Partnerships

A representative case:

- Kelun-Biotech × Merck (~$11B, 7 ADC assets)

Trends:

- Early-stage (Phase I/II) assets included

- Multi-target expansion (TROP2, CLDN18.2, c-MET)

- Bundled deal structures

➡️ Shift toward early innovation collaboration

Phase 3 (2025–Now): Platform-Level Collaboration

China ADC globalization enters a new phase:

- Platform licensing

- Multi-asset co-development

- Long-term strategic alliances

Examples:

- DualityBio × BioNTech

- Hansoh Pharma × GSK

➡️ Core value = technology platforms, not single assets

II. Key Drivers Behind Global Interest in Chinese ADCs

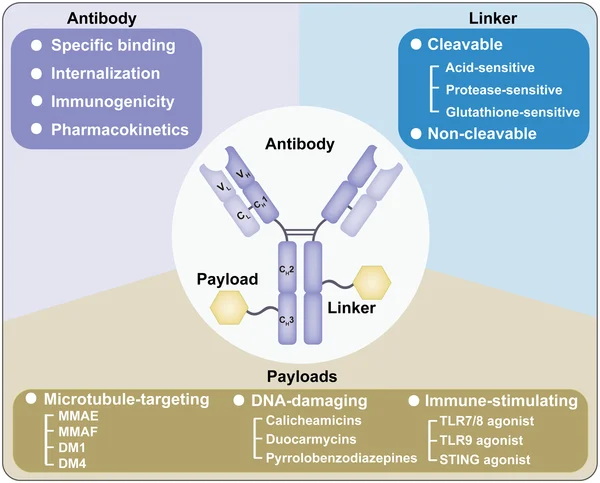

1. Full Value Chain Innovation

ADC development consists of:

- Antibody

- Linker

- Payload

China’s progress:

- Antibody → bispecific & multispecific

- Linker → improved stability & release control

- Payload → novel mechanisms (non-P-gp, immune modulation)

➡️ Transition: me-too → me-better → potential first-in-class

2. Differentiated Clinical Strategy

While global pipelines focus on:

- HER2

- TROP2

China is exploring:

- B7-H3

- CLDN18.2

- Novel bispecific ADCs

➡️ Focus on unmet clinical needs + differentiation

3. Clinical Development Efficiency

China offers structural advantages:

- Faster patient enrollment

- 12–24 month early validation timelines

- Lower early-stage costs

➡️ Reduced risk for global pharma partners

III. Structural Challenges and Risks

Despite rapid growth, several challenges remain:

1. Target Concentration

-

70% of deals focus on limited targets

- Risk of overcompetition & pricing pressure

2. Milestone Dependency

-

90% of deal value = milestone-based

- Upfront payments relatively low

➡️ Value realization depends on:

- Clinical success

- Regulatory approval

- Commercial performance

3. Limited Global Commercial Capability

- Most commercialization handled by multinational partners

- Chinese companies lack independent global infrastructure

4. Intellectual Property Constraints

- Linker & payload IP still dominated by global players

- Increasing risk of patent competition

IV. From Cost Advantage to Innovation Power

China’s ADC expansion reflects a broader shift:

- Cost-driven → innovation-driven

- Manufacturing advantage → R&D capability

ADC is only the beginning.

Future expansion areas include:

- Bispecific antibodies

- Cell therapies (CAR-T)

- RNA therapeutics

V. Further Reading

For a deeper analysis of ADC targets, pipelines, and approvals, see our detailed report on ADC drugs by target in 2026.

Conclusion

China’s ADC globalization is no longer about exporting individual drugs —

it is about exporting technology platforms and innovation capability.

As global collaboration deepens, Chinese biopharma is becoming:

- A core innovation contributor

- A strategic partner in global oncology development

DengYueMed will continue to track these trends and support the global distribution and accessibility of high-quality innovative therapies.