What Does Guideline Inclusion Mean? Analyzing the Demand Growth Path of Oncology Drugs

In the full commercialization process of innovative oncology drugs, regulatory approval only grants market entry. Inclusion in authoritative global oncology guidelines such as NCCN, ESMO, and CSCO represents the core inflection point for large-scale market volume growth.

Once a new drug is incorporated into clinical guidelines, it evolves from an investigational novel therapy into a standardized treatment option, fundamentally reshaping physicians’ prescribing logic, hospital medication structures, and overall market demand scale.

For pharmaceutical enterprises, medical institutions, and professional pharmaceutical circulation and commercial service platforms such as Dengyue Pharma, understanding the complete transmission mechanism of “guideline update — clinical implementation — demand expansion” is essential for judging product lifecycles and evaluating long-term market potential.

I. Underlying Logic of Guideline Dependence in Oncology Treatment

Oncology clinical practice relies far more heavily on authoritative guidelines than chronic disease management, driven by three industry-specific characteristics based on rigorous evidence-based medicine systems.

1. High Tumor Heterogeneity

The same cancer type contains multiple molecular subtypes with completely differentiated treatment regimens:

- Lung cancer: EGFR-mutant / wild-type

- Breast cancer: HER2-positive / HER2-negative

- Colorectal cancer: MSI-H / MSS subtypes

2. Rapid Iteration of Therapeutic Technologies

Oncology treatment has moved beyond traditional chemotherapy, with diversified innovative therapies continuously applied in clinical practice:

- Targeted therapy

- Immune checkpoint inhibitors

- ADC drugs

- Bispecific antibodies

- Cell therapies

3. Standardized Authority Required for Clinical Decisions

Oncologists worldwide primarily reference three core guidelines:

- NCCN (global standard)

- ESMO (European authority)

- CSCO (Chinese clinical practice guideline)

Essentially, guidelines convert massive clinical trial data into unified, executable standard clinical pathways, serving as the most authoritative clinical endorsement for drug efficacy.

Tumor heterogeneity, rapid technological iteration, and standardized clinical requirements jointly establish the absolute authority of clinical guidelines. Guideline updates constitute the fundamental institutional basis for the demand expansion of innovative oncology drugs.

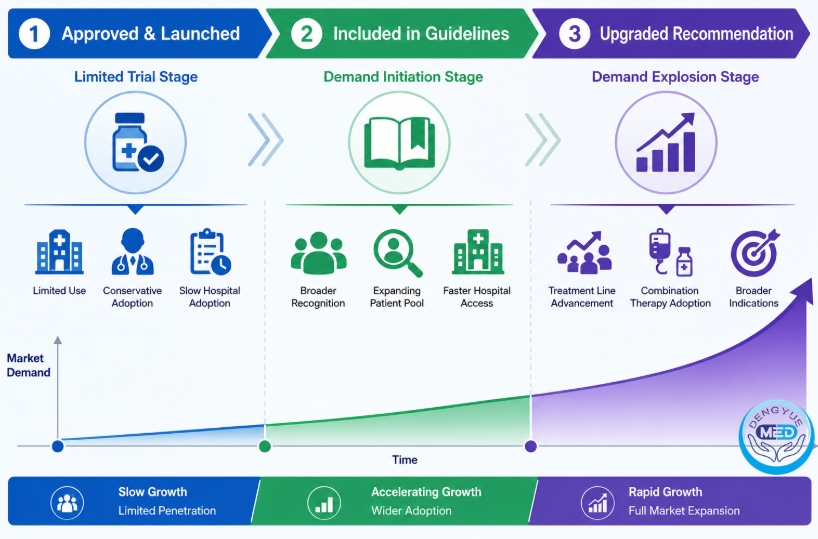

II. Three Lifecycle Stages of Innovative Oncology Drug Commercialization

Innovative oncology drugs follow a clear phased commercialization path from launch to full market penetration, with distinct clinical and market performances across stages.

1. Regulatory Approval: Limited Pilot Stage (Slow Growth)

Newly approved drugs only obtain legal qualification for clinical use and face multiple practical constraints that restrict large-scale demand generation:

- Limited coverage: Primarily available in tertiary oncology centers and trial-participating hospitals, with almost no penetration in grassroots markets.

- Conservative clinical adoption: Physicians remain observation-oriented with sporadic trial use, lacking standardized prescribing pathways.

- Delayed hospital access: Long pharmacy committee review cycles, incomplete medical insurance coverage, and slow updates to hospital procurement catalogs.

2. Guideline Inclusion: Demand Initiation Stage (Core Inflection Point)

Incorporation into authoritative guidelines marks the critical commercial watershed, unlocking incremental market space from three dimensions:

- Institutionalized clinical recognition: Drugs obtain industry-wide authoritative endorsement, upgrading from optional novel agents to standardized recommended regimens and shifting physician behavior from tentative trial to routine clinical application.

- Expanded eligible patient pool: The popularization of genetic and protein detection enables standardized screening at all hospital levels, significantly expanding the scale of treatable patients.

- Accelerated hospital admission: Guideline recommendations serve as core evidence for hospital pharmacy reviews, greatly shortening the cycle for drugs to be included in in-hospital and oncology-specific formularies.

3. Recommendation Upgrade: Demand Outbreak Stage (Full Volume Growth)

Therapeutic line advancement, combination regimen inclusion, and expanded indications drive exponential market growth with three core changes:

- Treatment line advancement: Second-line or later-line drugs upgraded to first-line preferred options, covering the largest population of treatment-naïve patients.

- Popularization of combination regimens: Combinations such as PD-1 plus chemotherapy and ADC plus targeted therapy become routine, increasing per-patient medication volume throughout the treatment cycle.

- Broader indications: Expansion from rare mutant subgroups to general populations and from single tumor types to multiple solid tumors, fully unlocking market ceiling potential.

The commercialization of innovative oncology drugs follows a clear progressive growth pattern. Post-launch trials deliver limited incremental gains; guideline inclusion breaks growth bottlenecks by consolidating clinical consensus and institutional access; recommendation upgrades trigger explosive growth through full-dimensional expansion of patient groups, clinical scenarios, and indications, forming a complete commercialization closed loop.

III. Differentiated Volume Growth Logic of Mainstream Oncology Drugs

Innovative drugs with different mechanisms of action exhibit distinct guideline-driven growth models, forming three mainstream industry paradigms.

Targeted Drugs: Substitution-Driven Growth

Represented by EGFR, ALK, and HER2 therapies.

These drugs directly replace traditional chemotherapy with standardized, well-defined clinical pathways, enabling stable and predictable first-line penetration and steady volume growth.

ADC Drugs: Pattern-Restructuring Growth

Mainly applied in breast cancer, gastric cancer, and non-small cell lung cancer.

With superior objective response rates, ADCs rapidly advance from later-line to frontline preferred regimens, reshaping traditional treatment paradigms and generating significant structural market increments.

Immunotherapy (PD-1/PD-L1): Overlay-Driven Growth

Evolving from monotherapy to chemotherapy combinations and multi-line, cross-tumor application.

Instead of replacing existing regimens, immunotherapy continuously expands market space by overlapping clinical scenarios, supporting longer lifecycles and broader market potential.

Key Takeaway

The three core oncology tracks demonstrate completely differentiated growth logic:

- Targeted drugs grow through stock-market substitution.

- ADCs deliver structural increments by restructuring treatment patterns.

- Immunotherapies expand continuously via scenario overlay.

Together, they define the mainstream growth paradigms for modern innovative oncology drugs.

Conclusion

The complete commercial growth path for innovative oncology drugs can be summarized as:

Regulatory Approval → Limited Clinical Trial → Guideline Inclusion → Recommendation Upgrade → Full-scale National Volume Expansion

Drug approval merely represents market entry qualification.

Guideline inclusion marks authoritative clinical recognition and the official start of demand growth.

Recommendation upgrades trigger explosive market expansion.

Guidelines define the theoretical market ceiling of oncology drugs, while professional service providers represented by Dengyue Pharmaceutical determine the actual realizable market value through channel layout, supply chain management, and commercial execution capabilities, bridging drugs from “paper recommendations” to widespread clinical adoption.

The commercialization of innovative oncology drugs follows a clear logic:

Clinical recognition defines market space, while implementation capability determines market realization.

Guidelines act as the core indicator of industry growth opportunities, while high-quality commercial and supply chain services serve as the ultimate guarantee for releasing the full market potential of innovative oncology drugs.